When it comes to streaming video’s shift to the platform era, I want to focus on Amazon. Throughout this mini-book, I’ve largely glossed over Amazon’s various video offerings and business models. This is because the company epitomizes the three eras I’ve described, demonstrates the importance of this final platform era, and also reminds us that there are no firm start nor end dates to an era—each one slowly grows as its predecessor recedes. With this in mind, it helps to tell a full history.

In 2006, Amazon launched Unbox, a transactional video store enabling customers to buy and rent movies and TV series, albeit through downloaded, not streaming copies. This was a classic “Access” offering and debuted a year after iTunes added download movie/TV purchase and rental capability to its otherwise music-centric store. In 2011, Amazon launched Instant Video, which enabled customers to stream a TV/film purchase or rental, while Prime Members could stream more than 30,000 titles for free. Again, both of these offerings were “late” to market, with streaming video and an all-you-can-eat library launching four years after Netflix and Hulu. In 2014, Amazon launched the Fire TV, a “connected TV” device that competed with Apple TV (launched in 2007), Roku (2008), and Chromecast (2013). That same year, Amazon bought Twitch, the market leader in live video game streaming. In 2016, Amazon launched Video Direct, which enabled independent content creators to upload their own videos to Prime Video and receive a prorated share of a royalty pool. Though Video Direct was the first streaming service to fold UGC video into a professional video streaming library, it launched more than a decade after YouTube, Google Video, and others. In 2019, Amazon launched Freevee, a free ad-supported streaming service, which came six years after pioneer PlutoTV, five after TubiTV, and two after The Roku Channel.

Although Amazon was typically late to a given Access innovation, it was the first to understand the criticality of originals. In 2011, Amazon began its originals strategy, the same year that Netflix commissioned House of Cards, which debuted in 2013, the same year as Amazon’s first originals, such as Betas and Alpha House. Over its first few years, Amazon was more cautious and slower than Netflix, but by 2015 its investments quickly began to ramp up. That year, Amazon bought the rights to The Grand Tour, the de facto spinoff to Top Gear, the most-watched series globally. In 2016, the service went global, with dozens of local market originals announced at launch. In 2017, Amazon made the most expensive TV rights deal in history (Lord of the Rings) and the first streaming-only major sports rights deal (NFL).

As we look back on the last decade, the growth of Amazon’s video business is extraordinary. In 2012, IDG and Ovum estimated that iTunes had a 50-70% share of the $2.5B digital TVOD market, while Amazon held 15–20%. By 2020, Amazon’s share had grown to 40%, while Apple’s had shrunk to that same level, in a market that had grown 5x during that same period. Although Fire TV launched eight years after Apple TV and seven after Roku, it became the largest connected TV platform globally by 2018; by 2022, it had matched Roku in the United States with 40% share each (this market is up about 10x since 2014). And although Amazon has single-digital share in smartphones and tablets, the company now sells one of every four SVOD subscriptions sold, and 1 in 3 that isn’t sold by the SVOD operator directly, generating billions in pure profit annually.

According to Variety, Freevee is now tied as the third-most-watched ad-supported streaming service. Amazon Video Direct has, however, not succeeded, though Twitch has successfully rebuffed YouTube and Facebook in the live gaming category. Prime Video sits at 8.7% of total streaming time in the United States (excluding UGC video), compared to market leader Netflix at 21% and runner-up Hulu at 9.6%, with Disney+ at 5.2% and HBO Max at 3.8%.

Originals have been instrumental to Amazon’s success in video. The clearest evidence here is the competitive response. After years of resisting the lure of original programming, Apple launched its own Prime Video–like service in 2019, with $2B in annual spending. Three years later, that sum had grown to $6–$7B, only 30% shy of Amazon in its ninth year. In 2021, Roku began its own originals strategy, too. And in 2022, Google bought the rights to NFL Sunday Ticket, the most expensive sports package on the market, for $2–$2.5B per year. Google had previously discussed buying these rights in 2013 (back when it was priced at $1.5B) but balked, believing that its Chromecast hardware and recommendations engines—access innovations, in other words—were sufficient.

But it’s wrong to think of Amazon’s original series and films as the driver of its other video businesses. Instead, they augment Amazon’s video flywheel. Every Fire TV helps to promote Prime Video (even if the Fire TV is bought so that a family can watch Netflix, YouTube, and HBO). But the more a user watches Prime Video, the more likely they are to buy SVOD subscriptions from Amazon and/or buy and rent from Amazon, which bolsters the use case for a Fire TV. And if a user already uses Prime Video, they’re more likely to buy a Fire TV, which also advantages Freevee. To frame this in a more abstract fashion: exclusive content drives hardware drives services drives third-party transactions, all of which drive greater lock-in and greater usage, and so on down the line. And all of this sits within Amazon’s broader flywheel, which includes one of the world’s largest advertising businesses (here, Freevee provides Amazon with not just more ad inventory to sell but also another ad format, premium video), the world’s largest ecommerce business (which is also advantaged by on-platform advertising), the world’s largest cloud business (which is advantaged by having more content to host and deliver), the world’s largest retail subscription (Prime, for which the benefits are obvious), and so on. There’s a reason absolutely everyone’s forecast for the winners of the “Streaming Wars” includes Amazon and Apple: they have too many points for leverage through which they can monetize a given film/series, and as long as they want to participate, they can afford to.

Another good example is Netflix. In 2017, the company released its first interactive series in Black Mirror’s Bandersnatch, which required programming “television” across interactive webpages using the open-source Twine tool. Four years later, the company added casual mobile games to its service, with AAA shooters added the following year. In 2023, the company confirmed reports that it was building a cloud game streaming service, a move that inevitably leads to the construction of a player network, communications suite, and microtransactions. In 2022, Netflix not only expanded to ads but also fitness programming partnerships with Nike, with live streaming events coming this year. For years, Netflix has been building up a merchandise and theme parks licensing business as well as activations and partnerships with retailers like Walmart. Many of these expansions are conventional to the video business (ads! live!), whereas others are conventional for anyone who owns franchises (licensing!), while still others take a more mixed (did Nike cover all or part of the cost for its series?) or pioneering (Netflix’s streaming service started as a free add-on to the DVD subscription; might games follow the same path?). Regardless, Netflix was originally positioned as a pure play streaming service, but every year, it seeks out new monetization models.

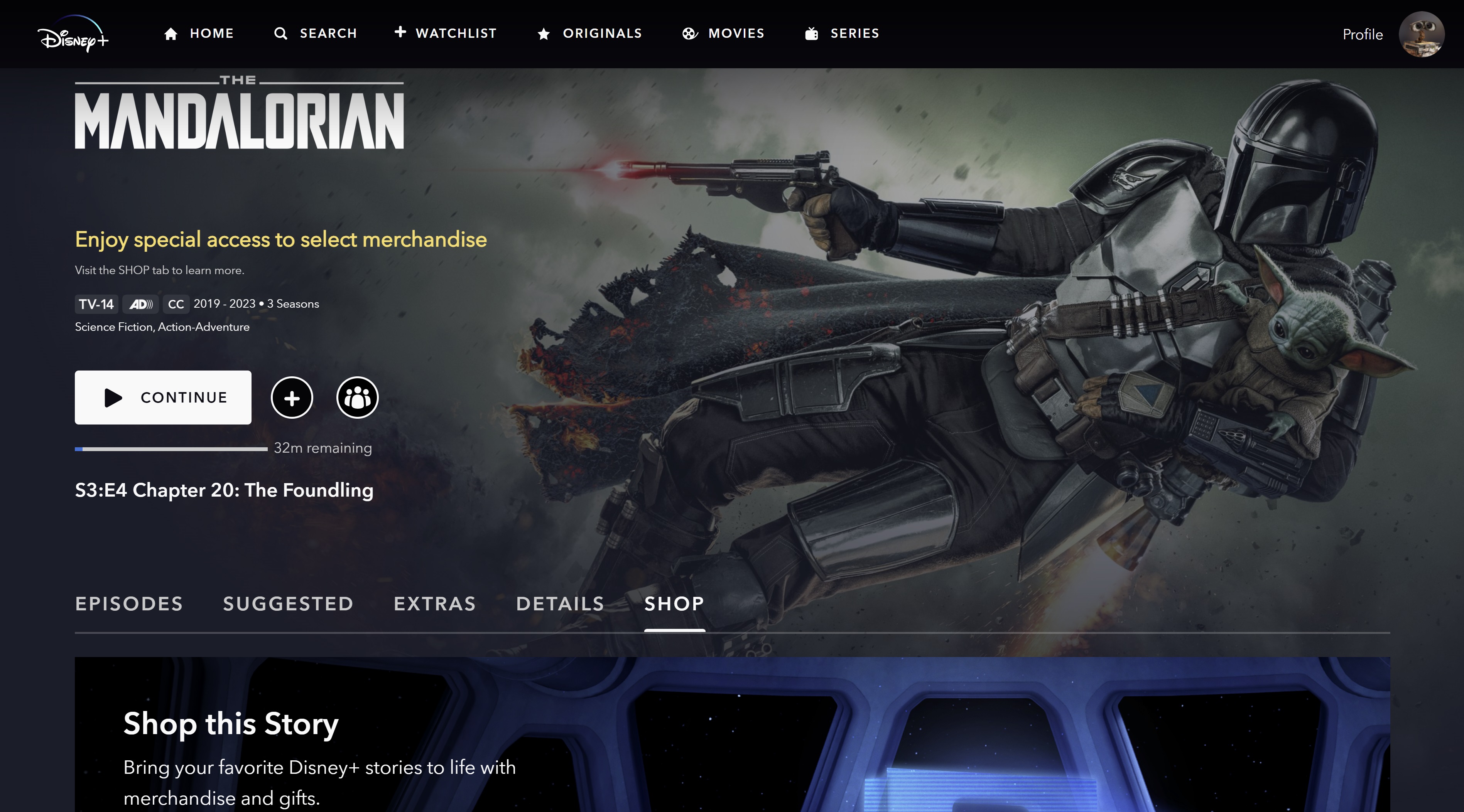

As the leader in multi-platform storytelling, Disney+ is the natural exemplar. In October 2022, the streaming service added a merchandise tab inside its application, enabling users to click from an episode list to behind-the-scenes extras, to buying a Baby Yoda toy or Elsa dress The next step is likely adding in-app purchase of movie tickets, followed by theme park passes and cruise ship vacations. While the functionality is basic, the financial upside is considerable—and far in excess of a $70 annual SVOD subscription which might, at best, deliver $20 in EBITDA. Disney would be able to cut out a greater share of transactions intermediaries, such as Walmart or Expedia. And with better targeting and personalization—that is, tailoring messaging and pricing to the Disney IP a family loves most—it’s easy to imagine greater upsell and cross-selling, too. In a sense, Disney+ would become the CRM for the entire Walt Disney Company.

The history of the “Platform Era” is short only because the era is new. As such, there's a limit to how much we can learn from today's movements and configurations. Instead, we should focus on how the dynamics of “streaming video” might change in the years to come—from who plays to how, where, and why.